The Best Solo 401k Providers in 2025

From flexible investment platforms to low-cost plans, these Solo 401k providers are leading the way in 2025. Find out which ones are worth your money — and your future.

John Angelo Yap

Updated May 16, 2025

Man typing on his computer, generated with Midjourney

Reading Time: 5 minutes

So you're a freelancer or small business owner trying to figure out retirement savings? I feel your pain. Choosing a Solo 401k provider is slightly overwhelming when you're trying to pick a provider that you'll want to be with for many years.

Some will nickel and dime you with hidden fees, while others restrict your investment options so severely you might as well be stuffing cash under your mattress.

But here's the good news: 2025 has brought some serious improvements to the Solo 401k landscape. Between fee reductions, expanded investment options, and better technology integration, there's never been a better time to set up one of the best retirement accounts in America

Solo 401k Plan Providers in 2025

Before diving into providers, let’s quickly cover why Solo 401k plans are SO POWERFUL for self-employed individuals and small business owners.

A Solo 401k lets you contribute as both the employer and the employee. That’s the magic behind why you can stash away so much—up to $70,000 for 2025 if you're under 50, and $77,500 if you're 50 or older (thanks to the standard catch-up contribution).

If you’re between 60 and 63, you can contribute even more—up to $81,250—because of a new, higher catch-up rule under the SECURE Act 2.0. That’s some serious tax-saving potential—top earners could be looking at over $27,000 in annual tax savings.

Here’s what makes Solo 401ks stand out from other retirement accounts:

- Higher contribution limits than most other retirement plans

- Flexible contributions – choose between pre-tax or Roth

- Loan access – borrow from your plan (IRAs don’t offer this)

- Minimal reporting hassle – no complex testing unless you hire employees

- Broad investment choices – from traditional assets to alternatives like real estate, depending on the provider

The Best Solo 401k Providers for 2025

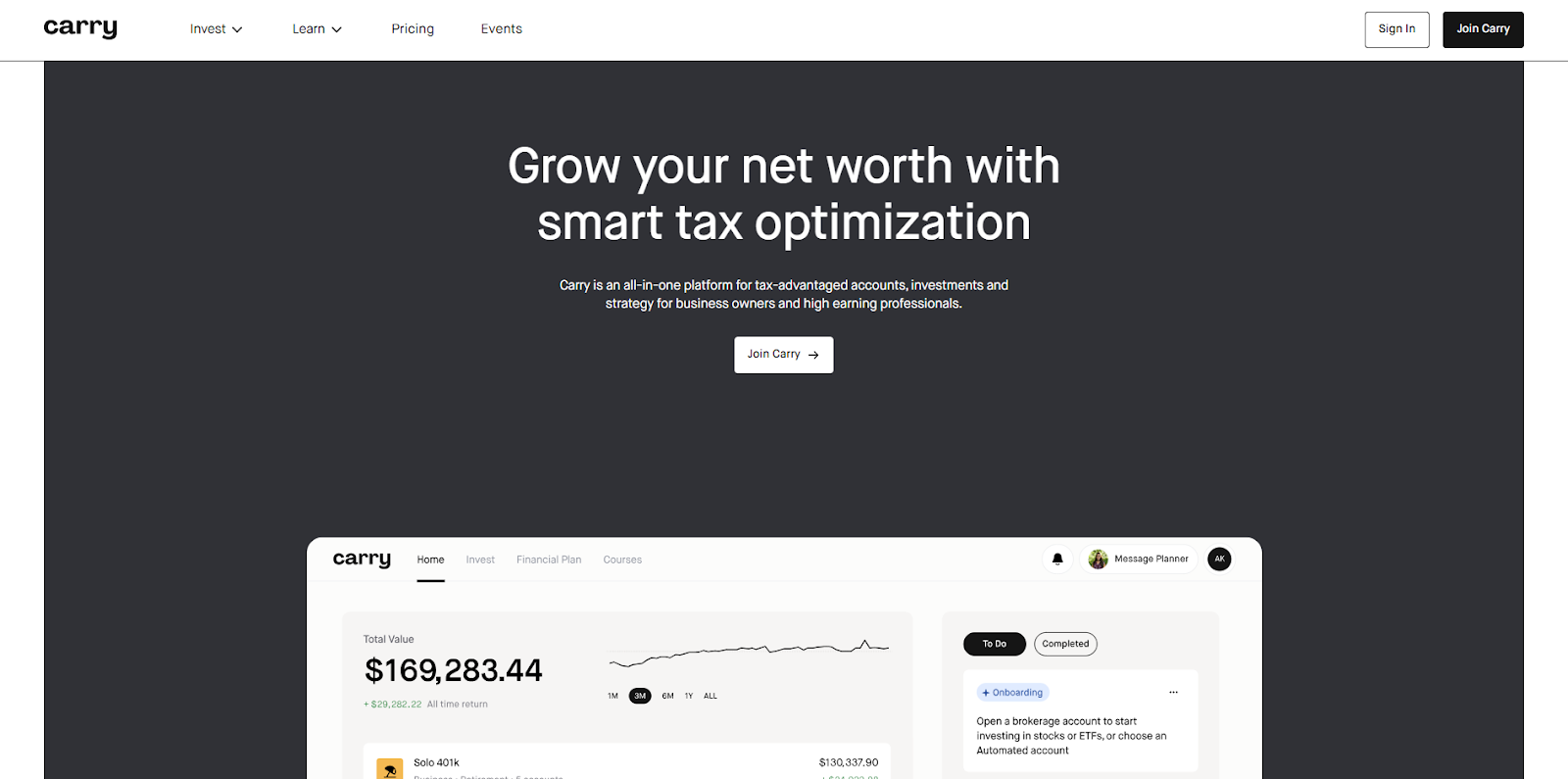

Carry

Carry has emerged as a standout provider in the Solo 401k space over the last few years. They focus on maximizing retirement savings with a tax-first approach.

Their platform is designed specifically for self-employed professionals and small business owners who want to supercharge their retirement contributions. From a user experience perspective, it's designed beautifully and super easy to use.

Key features of Carry's Solo 401k include:

- Mega Backdoor Roth capabilities in just a few clicks

- No hidden cash fees, transparent pricing structure

- Automated payroll integrations with services like Gusto

- Support for various business structures (S-Corp, PR, LLC, or Solo)

- Tax optimization tools to maximize your retirement savings

- Employer contribution calculator to help determine optimal contribution amounts

- Fast setup process

- Diverse investment options including stocks, ETFs, mutual funds, and alternatives

Limitations:

- Being newer to the market means less of a track record compared to established providers

Fidelity Investments

Fidelity remains a powerhouse in the Solo 401k space because of their other retirement accounts.

Key features of Fidelity's Solo 401k include:

- No account setup or annual fees

- $0 commission for most stock and ETF trades

- Extensive investment options

- Industry-leading research tools

- Mobile app access for account management

Limitations:

- No loan provisions — a major drawback for many freelancers

- Manual contribution process that doesn't adjust with income fluctuations

- Limited integration with modern payroll and accounting systems

Fidelity is ideal for those who want a trusted name and don't anticipate needing 401k loans or complicated automated contribution features.

Charles Schwab

Schwab continues to improve its Solo 401k offering, maintaining competitive positioning in 2025.

Key features of Schwab's Solo 401k include:

- No account maintenance fees

- $0 commission trading for stocks, ETFs, and Schwab OneSource funds

- Robust trading platform with excellent research tools

- 24/7 customer support

Limitations:

- No loan options available

- High fees for non-Schwab mutual funds (up to $74.95 per transaction)

- Manual funding requirements for both employee and employer contributions

Schwab works well for semi-retired professionals or those with stable income who prioritize investment research and trading capabilities.

E*TRADE

E*TRADE's Solo 401k offering has steadily improved, particularly in the loan administration area.

Key features of E*TRADE's Solo 401k include:

- No setup fees or account minimums

- Loan provisions available with streamlined paperwork

- Competitive investment options

- Advanced trading tools

Limitations:

- Annual administration fee of $25 per participant

- No automatic contribution adjustments

- Limited integration with accounting systems

E*TRADE is an excellent choice for active traders who also want the security of loan options.

New Trends in Solo 401k Plans for 2025

Everyone is trying to make the best product because they know you'll want to lock in a provider and stay with them for as long as possible. Here are some benefits of the newest providers:

- Tax optimization focus - Providers like Carry are emphasizing tax strategy as a core component of their offering.

- Automated integrations - Seamless connections with payroll systems and accounting software (Like Gusto) eliminate manual work and reduce errors. Carry does this.

- Mega Backdoor Roth simplification - What was once a complex strategy requiring multiple steps is now being streamlined by providers like Carry.

- Expanded alternative investment options - Beyond traditional stocks and bonds, providers are facilitating access to a wider range of investment vehicles. Like loans, crypto, etc.

The Bottom Line

The Solo 401k remains one of the most powerful retirement saving tools available to self-employed individuals in 2025.

While traditional providers like Fidelity and Schwab continue to offer solid options, innovative platforms like Carry are addressing specific pain points around maximizing contributions, tax optimization, and technology integration.

Before making your decision, take the time to evaluate how each provider handles:

- Maximum contribution limits and tax advantages

- Fee structures and hidden costs

- Investment options and restrictions

- Integration with your existing payroll and accounting tools

- Security measures and compliance

For business owners and self-employed professionals who want to maximize their retirement savings with a tax-first approach, Carry offers compelling advantages with their Mega Backdoor Roth capabilities and payroll integrations.

Whatever provider you choose, the most important step is to start saving now. The tax advantages and wealth-building potential of a Solo 401k are simply too valuable to ignore.

Want to Learn Even More?

If you enjoyed this article, subscribe to our free newsletter where we share tips & tricks on how to use tech & AI to grow and optimize your business, career, and life.